What really caused the $stETH depeg!

3AC x Celsius contagion

The Terra collapse, market-wide deleveraging, and now withdrawals from larger lending platforms have all worked to destabilize the stETH:ETH exchange rate in the past month. Also, a lot of misguided comparisons have been made, to compare $stETH to undercollateralized stablecoins like $UST.

So, before I explain what caused the depeg, I would try to clear the misguided comparisons by explaining what $stETH is.

$stETH is an ERC20 token that represents staked ether in Lido.

But what is Lido?

Lido is a platform that offers "liquid staking," in which users can lock any amount of ETH for validating purposes and then receive the stETH token, which can then be rehypothecated in DeFi to earn yield.

This $stETH token is a fully collateralized $ETH staked on the Ethereum PoS beacon chain. 1 $stETH = 1 $ETH staked. This means that when withdraws on the beacon chain are enabled, 1 $stETH can be redeemed for 1 ETH.

For the past few years, $stETH has had a lot of utility within the rapidly growing DeFi ecosystem. This is primarily due to its yield-producing nature. It comes with a native yield, which provides users/holders with yields that they would not get by holding $ETH alone.

Lido collects ETH deposits in a pool and distributes them to the co-validator operative's operators. The ETH is then staked to earn rewards. So, naturally, many will take the carry risk due to those yields.

It is important to note that there is no target price for $stETH.

This is because $stETH is based on the aToken standard, nominal balances are updated daily, with an oracle acting as a middleman.

Its primary purpose is to be collateralized regardless of how much the secondary market values it. The exchange rate between stETH:ETH reflects a fluctuating secondary market price rather than the underlying backing of your staked ETH. The ability to exchange your $stETH for $ETH on the secondary market is purely for convenience.

Because some participants require liquidity, the market is naturally seeking a fair price for stETH. This opens the door for others to purchase stETH at a significant discount.

As long as deposits are uncapped, $stETH will not trade at a value greater than 1 ETH. Because of arbitrage, if $stETH trades at 1.05 ETH, I can deposit 1 $ETH to Lido, receive 1 $stETH, and sell it on a secondary market for 1.05 $ETH, profit 0.05 $ETH, and drive down the price of $stETH.

This arbitrage currently only works in one direction, as $stETH is not yet redeemable. However, once it is possible, reverse arbitrage would be pretty straightforward.

If $stETH trades at 0.95 ETH, I can buy 1 $stETH for 0.95 $ETH, then redeem it for 1 $ETH, for a profit of 0.05 $ETH and pushing the price of $stETH up.

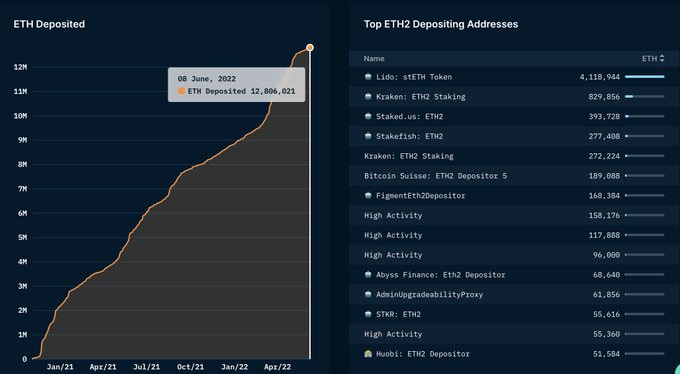

At the time of the depeg fiasco, 12.8 million ETH was in the ETH2 staking contract and Lido controls the staking rights to 32% of the 12.8 million ETH.

It is also important to note that after the merge, withdrawals of $ETH from the beacon chain will be disabled. It will only be available after the first hard fork, which is six to twelve months after the merge. Even after that happens, there would also be a withdrawal queue on the beacon chain. As a result, $stETH may not be redeemable for some time.

So, why did it depeg?

A few months ago, one of the most popular trades was to borrow ETH at 2% and do recursive farming or some form of stETH. This is because stETH was generating 4% yields, and on a massive loan book, stETH was one of the few ways to efficiently "generate" yield on ETH.

As a result, behemoths like Celsius went max long into this trade. But not only celsius. Basically, any large entities with loan books went long too. As a result, these organizations created a massive asset-liability mismatch.

While Luna and UST were both insolvent situations, stETH/ETH was not. It was in a liquid state, with a crisis of liquidity and confidence. The stETH is there, but the asset/liability mismatch in these lenders created a situation where they were forced to sell - just like LFG in LUNA.

These lenders have illiquid ETH on hand and owe liquid ETH that can be withdrawn at any time. If they halt withdrawals, they risk triggering a larger confidence crisis and a bank run. Given the massive loan books that these entities manage, stETH/ETH falling to 0.9 will cause significant pain.

This is because assets were recently marked down by 10% while liabilities remained unchanged. Lenders naturally have "thin" equity cushions in comparison to the assets they manage. This is how an illiquidity crisis becomes a solvency crisis.

So, people had reasons to be concerned. There was just too much $stETH floating around.

Then concern became panic, then people broke rank, and began selling.

This panic selling in $stETH eventually led to selling in ETH, thereby dragging down the entire crypto complex. There were already macroeconomic headwinds, and these structural selling flows swiftly exacerbated the crisis (depeg).

There could be several reasons why $stETH temporarily traded above/below its collateral value. The most obvious of them all is

FUD,

Liquidity premium

SC bug risk discount

Before the depeg of $stETH, Celsius, a notable crypto company happened to be running into liquidity issues. They held a significant amount of $stETH which was being used as collateral to borrow stablecoins. They also deposited $stETH as collateral on Aave, borrowed $ETH, deposited into Lido for $stETH, and created this yield loop.

Now, if they sold such an amount of $stETH, it would definitely cause stETH’s secondary market value to decrease.

Now, other market participants thought about this and decided to front-run Celsius by continuing to sell $stETH on the secondary market. This caused a liquidation cascade as some of the leveraged positions began to be flushed out by larger vulture-like market makers and manipulators.

On the other hand, regardless of how the secondary market values $stETH, it is still backed 1:1 by staked $ETH. Depending on your time preferences and risk tolerance, purchasing $stETH below its treasury value can result in a higher yield.

As Ethereum staking does not auto-compound yield, if you bought 1 $stETH while it was trading at 0.70 $ETH (30% discount) and Ethereum staking yield remains 4% APR, your aggregate yield will be 38 % APR after two years, rather than 8% as a normal staker.

But, given the liquidity dynamics of this investment, how much of a discount is reasonable? Is it worth the risk?

To be frank, we cannot explicitly answer this question, as it is more of a personal preference thing. The risk is not for everyone. But while a liquidation cascade won’t be pretty, it’s not a death spiral situation. This is because stETH pricing should be determined by four factors:

The market's current desire for liquidity (Demand/Supply)

Current market volume and liquidity

Chances of a successful/delayed merger

The dangers of smart contracts

i. The market's current desire for liquidity (Demand/Supply)

Demand for liquidity ebbs and flows at various stages of the market cycle. When prices are rising and liquidity is high, it is simple and inexpensive to liquidate positions, and vice versa.

Liquidity is ephemeral. It can come and go. Asset liquidity can increase or decrease with what’s going on in the market. One day, it can be easy to sell, and the next day hard. Or one day, it can be easy to sell but hard to buy, and the next day easy to buy but hard to sell.

During the depeg, Amber, for example, with over $140 million in its wallet, withdrew from the curve pool. Being a large player, it was indicative of potential larger sell pressure brewing.

But Celsius is the most important supply/demand factor in this case. If one believes Celsius will become a forced seller, the supply/demand balance will be drastically altered, as highlighted above. The key question now becomes how much of the $stETH can be absorbed by the market, and at what cost.

So, how liquid is stETH exactly?

ii. Current market volume and liquidity

To answer the question above, we have to look at the market volume and liquidity of the depeg timeframe. At that time, the total liquidity in the pool had dropped by more than 20% in the early hours of the morning, owing to significant selling from wallets associated with Alameda and Celsius.

The first stage of the avalanche attack on UST was the withdrawal of liquidity from the three pools. Less liquidity = More risk.

When combined with Amber's withdrawal of over $150 million in stETH liquidity, it was most likely a forewarning to sell. That's $150 million that could hit the market in the coming days.

Finally, liquidity runs out. Whales and smart money were now selling. In that single month, the amount of stETH held by Smart money wallets decreased from 160,000 stETH to 27,800 stETH.

In fact, Alameda dumped 50,615 stETH into the market over the course of two hours on that Wednesday.

The point is that, due to the closed-ended liquidity structure of stETH, some institutions and ordinary participants were exposed to it at an incorrect risk level. When those tokens hit the market, they had the potential to cause significant damage.

iii. Chances of a successful/delayed merger

The next risk was the possibility of a delay, or even failure, of the beacon chain, which would have an impact on stETH. Remember that stETH is similar to an ETH future.

The expiration date is currently unknown, but we do know that withdrawals will be disabled for at least 6-12 months following the merger. Furthermore, only 4-5 validators may withdraw per epoch (6.5 minutes). As a result, if every locked ETH attempts to withdraw, the entire queue process will take 1.4 years.

In this sense, if the merge is delayed and ETH retrieval takes 6-12 months after the merge, having your tokens locked incurs an additional liquidity cost that is far greater than the yield earned during that period.

iv. Smart contract risk

A smart contract risk exists in addition to any demand/liquidity/merge risks. Based on the insurance costs of Lido deposit contracts on Nexus mutual, which stand at 2.6%, this is fairly simple to price.

At the very least, the smart contract risk in stETH is 2.6%, which is roughly the current stETH/ETH discount. This indicates that the stETH risk is vastly underpriced.

GBTC is a similar case to how stETH could be priced in that it is an investment in closed-end protocols/funds.

Because it is a closed-end fund, you must sell your GBTC position on the secondary market. Secondary markets are the only source of liquidity until it is converted to an ETF. If you want to sell your stETH, you must do so on the secondary market until the coin merges.

In both cases, the asset's fair value market price is determined by liquidity, open-end risk, and supply/demand dynamics. But, in this case, why does one trade at a 3% discount while the other trades at a 30% discount when the former has added smart contract risk with Lido?

In retrospect, it appears that they cut losses at a good absolute level through what appears to be June at around 2.8-3 USD per share. A very manageable hit of ~$100m for their clients.

When huge lenders fail, the ecosystem suffers because they have a complex web of transactions with other players. The risk of a third party becoming involved becomes real. Credit contracts as loans must be repaid and assets must be sold for cash.

What's the point?

A number of the game's biggest players are frequently incorrect, and in this case, some entities have completely mispriced the cost of liquidity in both GBTC and stETH, resulting in a liquidity black hole in both cases.

Finally, in response to Lido and others. We believe that the one-year staking yield for this liquidity trap is simply too low. Perhaps that figure is similar to GBTC's 30%, or perhaps it is higher due to market participants being forced sellers. However, it is not 3%.

Despite that, we do believe that people would gladly buy stETH at any price. But when you add in an indiscriminate, forced seller, the dynamics shift slightly.

The forced seller is the result of liquidations (if any) and, possibly, Celsius.

Let's dig in…

Now, it is important to remember that Celsius Network, is one of the crypto lenders facing liquidity troubles in the industry's ongoing credit crisis.

Recently, a wallet linked to Celsius transferred $81.6 million in USDC to the automated decentralized lending protocol Aave, according to blockchain transactions. Celsius's debt to Aave was reduced to $8.5 million as a result of the transaction.

Crucially, the transfer released over $500 million in stETH. This made Celsius one of the largest single holders of stETH. Now, this Celsius stake represents almost a tenth of $stETH's total market capitalization, at $4.4 billion.

But there’s an issue here.

According to digital assets data provider Kaiko, there is insufficient liquidity in centralized and decentralized exchanges for troubled crypto lender Celsius to sell their $stETH tokens on the open market, leaving over-the-counter (OTC) transactions as the only option.

Simply put, a sale of the magnitude required by Celsius would not be possible without nuking the price of $stETH.

We were able to calculate Celsius' assets and liabilities using on-chain analysis. Here's how it works: With $3.48 billion in total assets and $1.11 billion in loans, we have $2.374 billion in equity (this assumes Celsius owns 45% of the circulating supply of their CEL token, or $100 million).

Using their known DeFi wallets, The complete list of assets is available here:

The important thing to remember here is that Celsius is a HUGE holder of stETH. In fact, they are the largest holder of stETH that pays interest (stETH on Aave).

When we look specifically at Celsius' ETH holdings, we see that 71% is in illiquid/low liquidity types.

$510 million in ETH is locked in the ETH2 staking contract and cannot be accessed until after the merge.

$702 million is in stETH, which is difficult to exit through liquidity pools.

So, what happens if Celsius depositors want to cash out? Have they redeemed themselves? Why are 'HODL Mode' settings enabled on accounts?

Following the Terra meltdown (May 6th-12th), there was a $750M outflow of funds (150M ETH & $150M BTC). Celsius experienced $450 million in net outflows in the last two weeks of May. Even if we exclude the week in which outflows were not reported, Celsius experienced $1.2 billion in outflows.

Such outflows raised the possibility of a bank run on Celsius Network. The graph below depicts outflows over the last five weeks. The total amount of ETH withdrawn between the 22nd of April and the 26th of May was 190k. In comparison to the previous 5-week period (between the 18th of March and the 21st of April), Celsius saw 50k inflows.

Conclusion:

Generally, Celsius has seen a large number of withdrawals for their ETH and assets. So, they had to come up with a safety measure for their company. They have currently enabled "HODL mode," which prevents users from withdrawing funds from the Celsius network.

The long-term impact of Celsius failure is unknown...but crypto prices will undoubtedly continue to fall, as money exits the system.

Yes, Celsius rose $700m last year. However, they suffered significant losses as a result of various hacks and incidents.

Whoever panics first, panics best. There is no benefit to holding assets with celsius. If you can, get out.