The Case for Reevaluating Ragequit Fees and Unlocking Liquidity in Frax Protocol

The Case for Reevaluating Ragequit Fees and Unlocking Liquidity in Frax Protocol

A possible/sustainable profit strategy?

Have you ever tried selling a token on a Dex and it couldn’t go through because there was no liquidity?

Yeah, frustrating right?

Liquidity pools play a vital role in providing stability/efficiency in Defi trading. Now, the Frax Protocol has been a prominent player in the world of decentralized stablecoins, offering stability and liquidity to its users. It has been at the forefront of discussions on liquidity management, unlocking mechanisms, and fee structures.

However, the question of whether users should be allowed to ragequit from low Total Value Locked (TVL) pools has sparked a spirited debate within the Frax Finance community. Initially designed as an emergency exit for liquidity providers, clever strategists within the Frax community are now exploring its potential as a profit mechanism for the protocol.

Today’s article delves into the various perspectives surrounding the implementation of the ragequit function and its potential as a profit mechanism for the protocol.

Let’s dig in…

How it all started:

The current discussion revolves around the issue of low Total Value Locked (TVL) pools with Annual Percentage Rates (APRs) significantly lower than inflation. The argument here is that an escape hatch, such as a ragequit option, should be implemented to allow users to rebalance their locked stakes.

To strike a balance, it is suggested that a ragequit option be made available for all pools, with the fee adjusted on a per-pool basis. Pools providing substantial liquidity and protecting the peg should have higher fees, ensuring a proportional commitment from stakers.

In DeFi, "ragequitting" refers to the act of prematurely withdrawing funds from a liquidity pool or protocol. It occurs when participants exit due to dissatisfaction with returns, perceived risks, or unfavourable changes.

But the issue with ragequitting is its impact on liquidity and protocol stability. So, addressing these concerns behind ragequitting is crucial for user empowerment and protocol growth.

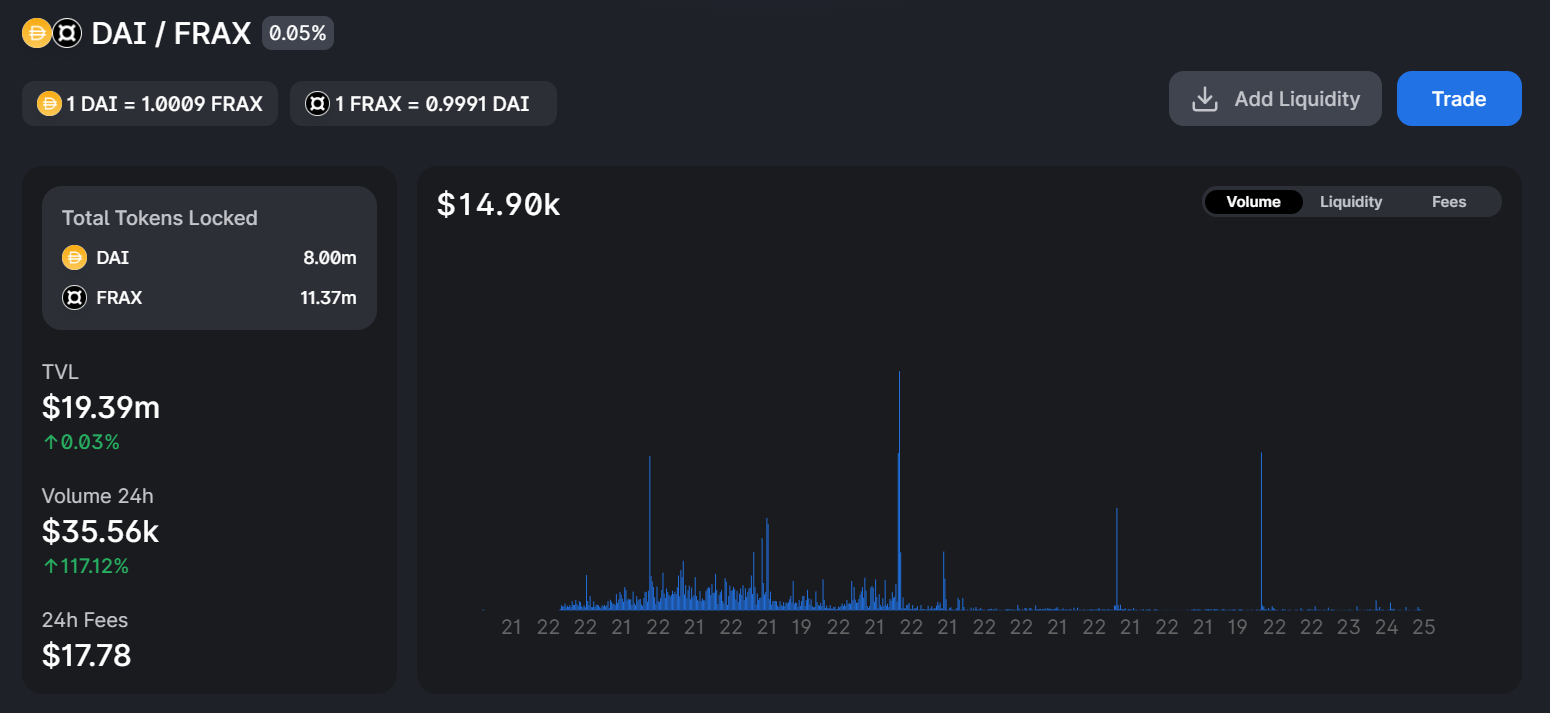

One particular pool that has been at the centre of this discussion recently is the Gelato Frax/DAI pool, which had $2.9M liquidity and sees only $10K volume per day. Outside of the Gelato pool, we still have the original Uniswap FRAX/DAI pool, which has $16.9M liquidity.

With $19.39 million in liquidity but only $35.56k in daily trading volume, some argue that this pool serves little purpose beyond locking a small amount of liquidity for Frax. Just look at the fees. A measly $17/D? So, why not allow users to exit this pool and possibly generate an additional $600,000 in profits for the protocol?

So, what is the case here?

The case for reevaluating ragequit fees and unlocking liquidity in the Frax Protocol is based on the potential for generating additional profits and achieving a 100% Collateralization Ratio (CR) swiftly. By allowing users to leave low Total Value Locked (TVL) pools through the ragequit function, the protocol can unlock liquidity and redirect it towards raising the CR.

What is a Ragequit function?

The Rage Quit function is a mechanism that was originally introduced as a safety measure for liquidity providers who wished to exit a liquidity pool early. It allowed them to withdraw their funds by paying a penalty fee, incentivizing long-term commitment to the protocol.

The Ragequit Fee:

A "ragequit fee" is a fee or penalty imposed on participants who choose to utilize the ragequit function in a decentralized finance (DeFi) protocol.

The purpose of a ragequit fee is to discourage impulsive exits and ensure the sustainability and stability of the protocol.

Ragequit fees serve as a mechanism to align the interests of participants with the long-term health of the protocol.

The Benefits of Rage Quitting for Frax Finance:

Allowing users to leave low-TVL pools would boost profits towards achieving a 100% Collateralization Ratio (CR) swiftly.

Capitalizing on this opportunity will unlock liquidity and redirect it towards raising the CR.

Concerns about ragequitting for Frax Finance:

Potential profits are enticing, but they worry about the impact on liquidity and stability of the Gelato Frax/DAI pool.

A significant outflow of liquidity from numerous users ragequitting could disrupt trading and challenge the protocol's peg.

Solutions…

In the subsequent discussion on the Frax Finance telegram group chat, one of the key ideas proposed by community members is the implementation of dynamic unlocking fees. Rather than applying a fixed percentage fee across all pools, this approach suggests varying the fee based on factors such as lock time, pool liquidity, and historical performance.

Such a dynamic fee structure would incentivize liquidity providers to commit to longer-term lock-ins in larger pools, promoting overall protocol stability while providing a pathway for profit potential.

Let's take some examples …

Imagine that Frax Finance introduces a dynamic unlocking fee structure for its liquidity pools. Maybe looking at the fees this way…5% - 1Y, 10% - 2Y, 15% - 3Y or something like that would be better…Because 20% may be reasonable for some that are locked between 2 and 3 years to unlock it at this rate but it certainly isn’t gonna be reasonable for a lot of people that only have a lock time left of 1 and a half years.

![Image - 144442] | Rage Quit | Know Your Meme](https://substackcdn.com/image/fetch/f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F8055e861-7e6d-4f6e-9be3-50988a69f6dd_750x600.jpeg "Image - 144442] | Rage Quit | Know Your Meme")

A large and well-established pool with significant liquidity and a long lock time might have a lower rage quit fee, let's say 5%, encouraging liquidity providers to commit to long-term engagements. On the other hand, a smaller pool with lower liquidity and a shorter lock time could have a higher fee, such as 15%, discouraging frequent exits and promoting stability.

Scenario: A liquidity provider in the large pool notices an attractive investment opportunity outside the Frax protocol. Instead of withdrawing their funds without penalty, they decide to stay locked in, leveraging the lower fee for potential future profit. This not only aligns with the provider's interests but also ensures that the pool's liquidity remains stable, benefiting the overall ecosystem.

Another intriguing proposal revolves around utilizing the Rage Quit function to capitalize on market opportunities. By allowing liquidity providers to exit their positions at a cost, the Frax protocol can unlock idle funds and deploy them into higher-yielding strategies or investment opportunities.

For instance, during market downturns when stablecoin yields are high, liquidity providers might opt to rage quit, releasing their funds to capitalize on these opportunities. Once market conditions improve, they can re-enter the protocol at potentially higher yields, thus generating a profit for both the provider and the protocol.

Balancing Incentives: Ethical and Long-Term Engagement

While unlocking profits through the Rage Quit function holds immense potential, maintaining ethical incentives and long-term commitment remains a crucial consideration. To strike a balance, community members have suggested that certain unlock reasons should be considered valid. These might include seeking better investment opportunities, capital reallocation, or the expiration of a fixed lock-in period.

For example, wanting to reallocate capital or earning a reasonable profit should be valid reasons for unlocking locked stakes. For instance, a 10% profit is deemed a valid unlock reason, especially in cases where minimal adoption and defence against a bank run are the only motivations for locking.

I believe that it is crucial not to punish liquidity providers for valid unlock requests, as it could discourage future participation and harm the overall protocol. Setting a rage quit fee that aligns with these valid unlock reasons could provide liquidity providers with a fair and transparent option to access their funds while safeguarding the protocol from sudden liquidity shocks.

You can see who used the ragequit function here:

Approximately $200,000 has decided to leave in frustration. Consequently, gaining the protocol around $40,000 in profits. It is likely that more individuals will follow suit when the market experiences a downturn, and they desire to deploy their stable assets. Perhaps in the future, Fraxchain might incorporate a ragequit function if demanded by its veFXS holders, similar to frxETH redemptions.

Of course, this would be implemented as long as the protocol remains profitable from it. The ultimate goal is to achieve a 100% collateralization ratio (CR) promptly, allowing the allocation of resources to more beneficial endeavours. Moreover, reaching 100% CR will help eliminate much of the unnecessary fear, uncertainty, and doubt (FUD) surrounding the project.

Thinking about it, as long as the ragequit fee is larger than (1-CR) (the actual breakpoint depends on what the LP consists of), it should be pretty good for FXS holders. Right now (1-CR) ~= 8%. Although for it to be truly fair, one would also need to take into account how much additional FXS the lockers managed to farm compared to non-lockers.

If Frax should eventually go this route, then I suggest implementing an automated unlock process based on the gauge voting system. This way, clear rules would govern stakers and protocols, minimizing the need for a heated governance process for each unlocking event. Such a system would allow stakers to react to risk and drive liquidity in line with gauge voting, ensuring a dynamic and adaptable ecosystem.

TL;DR:

The idea is for Frax Protocol to consider allowing users to exit low Total Value Locked (TVL) pools through the ragequit function for profit potential and achieving a 100% Collateralization Ratio (CR).

Implementing dynamic unlocking fees based on factors like lock time and pool liquidity could incentivize long-term commitments and stability.

Unlocking liquidity could boost profits and redirect funds to more profitable opportunities during market-driven scenarios.

However, this strategy must balance user incentives with the protocol's stability, as significant liquidity outflows may disrupt trading and challenge the peg.

Valid unlock reasons, like seeking better investments, should be considered ethically to encourage liquidity providers without discouraging them.

Governance processes should carefully consider profit strategies to ensure the protocol's sustainability and long-term health.

Success depends on market conditions, and the strategy may vary in attractiveness during periods of high market volatility versus stable conditions.

Conclusion

I believe that the debate surrounding the ragequit function as a profit mechanism for Frax Finance pools is geared not only to the potential for generating additional profits but also expediting the achievement of a 100% CR.

Though not everyone agrees, to my thinking, Frax Finance has proved her resilience and continues to evolve and innovate, and I believe the exploration of the Rage Quit function as a profit mechanism is a testament to the dynamic and engaged community.

Maybe by implementing dynamic unlocking fees and leveraging market-driven opportunities, Frax Finance can potentially boost protocol profits while providing liquidity providers with greater flexibility. Frax Finance can pave the way for a groundbreaking profit mechanism that benefits all stakeholders in the ecosystem.