Lessons from Technova

Why Africa's blockchain thesis should be Credit not Payments

Last weekend, I was in Ebonyi for Technova 2026.

For context, Ebonyi is not Lagos. It is not Abuja. It is a state in the southeastern geopolitical zone of Nigeria, landlocked, predominantly rural, and ranked among the lowest in the country on most economic indices. Its economy runs on salt mining, rice farming, and limestone extraction. Enugu and Abakaliki are the closest reference points most Nigerians reach for when they think of that part of the country. Blockchain is not the first thing that follows.

That geographic and economic context matters because it tells you something about who was in the room. These were not the crypto-native Lagos traders who have been moving stablecoins since 2020. These were not Abuja policy people hedging their bets on the next regulatory cycle. The people asking questions at Technova were asking them from a position of genuine distance from the industry, which meant the questions were honest. The energy in that hall was so beautiful to see, and that is exactly what made it worth the trip.

I was on the panel for “The Impact of Blockchain Adoption in Africa,” with four questions rotating among the speakers.

The ones I kept coming back to in my head, even after the event, were: what does blockchain actually solve for us, and what misconceptions about blockchain adoption in Africa need to be corrected?

Here is what I said, and I will stand by it:

…We keep celebrating adoption metrics that do not translate into economic leverage for Africans. P2P volume, stablecoin usage, and wallet downloads. These are real, but not what we should be after.

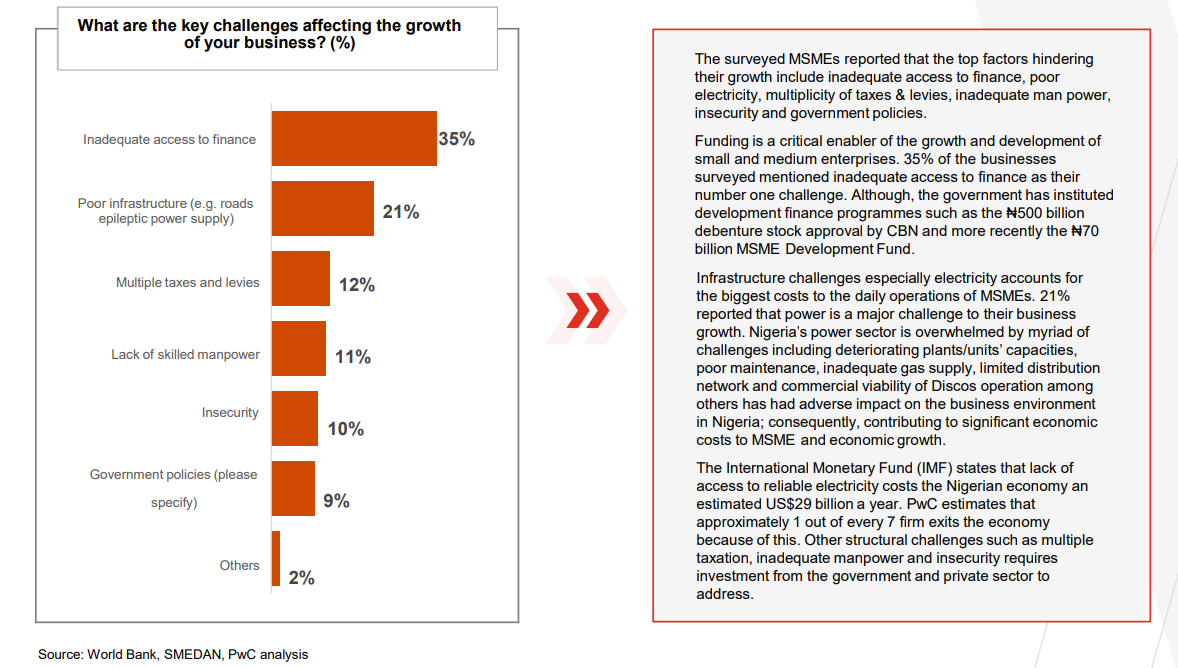

Africa has a credit gap estimated at over $400 billion for SMEs alone. That number is massive. Banks will not lend because they cannot price risk on borrowers who have no formal credit history, no titled collateral, and no paper trail that legacy financial infrastructure recognises. So the capital sits on one side of a wall, and the businesses that need it sit on the other side, and nothing crosses.

That is why when I hear people say the African blockchain thesis is payments, I know they have not thought it through. Payments are the entry point. Credit is the thesis. And almost no one is building toward it…

What Credit Actually Is

The word “credit” is used loosely. In colloquial use, it means borrowing money. In economic terms, credit is the mechanism by which future productive capacity becomes present capital.

A trader has a contract to supply 500 cartons of goods next month. He/She has the relationships, the logistics, and the buyer. What they lack is the working capital to purchase the inventory today. Their future productive capacity is real, but without credit, it remains locked in the future. With credit, it becomes operational today. The transaction happens, the employment it generates happens, and the tax revenue it creates happens.

This is why I do not see credit as a financial service in the narrow sense. To me, it is a form of time-compression mechanism that allows economies to move faster than what the accumulation of savings would otherwise permit. Every developed economy in history has grown, in significant part, by expanding access to credit. e.g., the United States institutionalised the 30-year fixed-rate mortgage after 1934 and converted future income into present home ownership at scale. South Korea used directed credit to compress what would have been decades of industrial accumulation into roughly 20 years. POSCO, Hyundai, and Samsung were built substantially on state-channelled credit, not retained earnings. Germany’s Mittelstand, its famed SME backbone, was a credit infrastructure product before it was an industrial one.

If you notice the pattern here, it is that productive capacity was deployed ahead of savings accumulation, and the economy moved faster because of it. Thus, the question for Africa is not whether credit matters, but why the infrastructure to deliver it has not been built.

From my perspective, the answer is that the infrastructure used to assess creditworthiness was built for a different borrower profile, in a different market, under different assumptions. It does not fit with our realities. And rather than build new infrastructure, the formal financial system has largely opted to exclude the borrowers it cannot price.

What an MSME Is, and Why It Carries the Continent

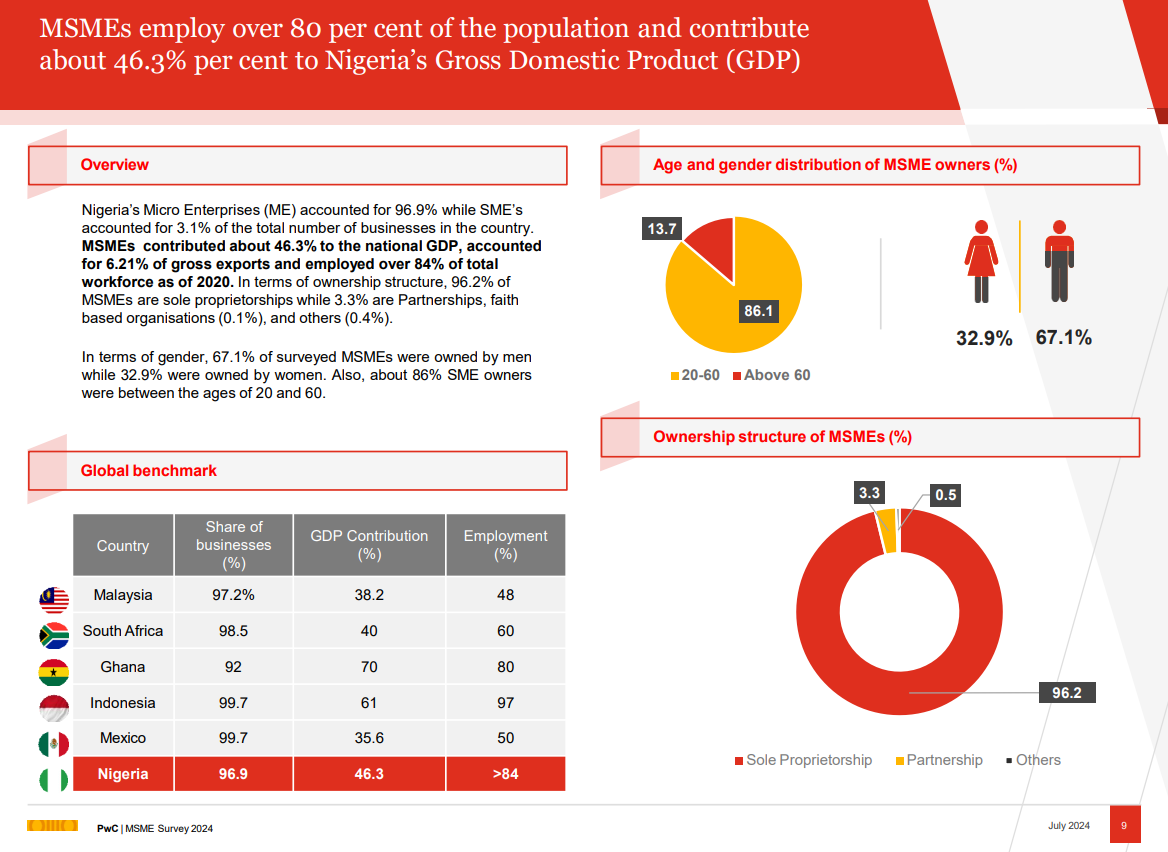

MSME stands for micro, small and medium enterprises. The definition varies by jurisdiction, but in Nigeria, the Small and Medium Enterprises Development Agency of Nigeria (SMEDAN) defines micro enterprises as those with fewer than 10 employees and assets below N5 million. Small enterprises employ 10 to 49 people, with assets between N5 million and N500 million. Medium enterprises employ 50 to 199 people, with assets up to N500 million.

Those definitions are technical and arguable, but that is not the point I want to make today. The point I want to buttress is the economic reality they describe.

The MSME sector in Nigeria employs approximately 84% of the labour force and contributes nearly 48% of GDP. Africa-wide, the picture is structurally similar. The International Finance Corporation estimates the SME financing gap on the continent at over $400 billion annually. The figure covers the gap between what SMEs need to grow and what formal financial institutions are willing to lend. It is not a measure of demand by firms that banks have evaluated and rejected. A significant portion of that gap represents firms that never applied, because they already know the outcome.

The Nigerian SME sector cannot be understood without understanding the informal economy. The National Bureau of Statistics estimated in 2019 that the informal sector contributes roughly 57% of Nigeria’s GDP when measured using a revised methodology that accounts for unrecorded activity. Many of the 41 million MSMEs that SMEDAN counted in its 2021 national survey operate entirely outside formal registration, tax filings, and financial records.

This is not evasion, but a rational response to a system where formalisation offers few tangible benefits and imposes real compliance costs. A market trader in Onitsha or a spare parts dealer in Ladipo does not incorporate because incorporation does not improve his access to capital, reduce his tax burden, or give him recourse to a legal system he can afford to use. He operates informally because the formal system has not offered him a compelling reason to join it.

The consequence is a borrower who is invisible to legacy credit infrastructure. No tax records. No audited accounts. No registered assets. No formal employment history. From the perspective of a bank’s risk model, he does not exist as a creditworthy entity. From the perspective of the actual economy, he is one of its primary engines.

Why Formal Lenders Cannot Solve This

Banks are not being negligent. They are rational actors operating legacy risk infrastructure built for a different borrower profile. The tools that banks use to make lending decisions presuppose three things: a credit bureau that has recorded the borrower’s repayment history, titled collateral that can be legally seized and liquidated in the event of default, and auditable financial records that allow a loan officer to model repayment capacity.

In Nigeria, credit bureau coverage is limited. TransUnion and CRC Credit Bureau operate, but their data skews toward borrowers who have already engaged with the formal financial system. The borrower who has never had a bank loan, a mobile credit product, or a formal trade credit arrangement does not exist in their databases. There is no negative record on him/her. There is no positive record either. He/She is a blank file, and a blank file is, by default, high risk.

Titled collateral is a deeper problem. Land tenure in Nigeria is governed by the Land Use Act of 1978, which vests all land in the state. Individual occupancy rights are issued as Certificates of Occupancy (C of O), but the process for obtaining one is slow, expensive, and often politically mediated. The majority of land in Nigeria is held under customary tenure arrangements that predate the Land Use Act and operate outside its formal framework. Customary land cannot be offered as collateral in a formal lending transaction because a lender cannot obtain a charge over it that a court would enforce.

The result, then, is a structural exclusion that has nothing to do with the borrower’s creditworthiness and everything to do with the design of the credit infrastructure. Thus, we can conclude that the wall between capital and the businesses that need it is not built of risk, but of incompatible data formats.

Why Payments Are the Entry Point, Not the Thesis

Africa leads global rankings in peer-to-peer crypto trading volume. Nigeria has ranked first or second on Chainalysis’s Global Crypto Adoption Index for multiple consecutive years. Stablecoin usage for remittances and cross-border trade settlement has grown materially, particularly in corridors where banking rails are slow and expensive. This is real progress.

But the payments thesis has a ceiling, and it is worth stating clearly what that ceiling is.

Payments move value. They do not create it. A trader who uses USDT to pay a supplier in Guangzhou, rather than using a correspondent bank, has saved on fees and settlement time. He/She has not acquired leverage. Their balance sheet is the same size after the transaction as before it. The payment was more efficient, but their capacity to grow was not expanded.

Credit expands productive capacity. A loan of N5 million to a food distributor in Aba does not just move N5 million. It enables a transaction that generates margin, employs workers, pays suppliers, and creates tax revenue. The loan is retired from the proceeds of the activity it financed. The economy is larger after the credit event than before it. Payments cannot do this. Only credit can.

If you ask any payments maximalist out there, their position would implicitly assume that efficiency is the binding constraint on African economic participation. But it is not! The binding constraint is capital access. An MSME that can send payments faster is a faster version of the same-sized firm. An MSME that can access credit against its verified history and assets is a larger firm. Those are categorically different outcomes.

Blockchain > Payments > Credit

What Has Been Tried, and Why It Stalled

The idea of using blockchain infrastructure to extend credit to underserved borrowers in emerging markets is not new. Several protocols have attempted it, and I’ll briefly discuss their outcomes to reveal the specific failure modes that an Africa-specific stack must avoid.

Goldfinch: Goldfinch launched in 2021 with the premise that there was DeFi capital sitting idle in developed markets, and there are creditworthy borrowers in emerging markets who cannot access it. They tried to be that bridge.

Goldfinch did not lend directly to end borrowers. It lent to local lending businesses, called Borrower Pools, which then on-lent to individuals and SMEs in their respective markets using their own underwriting processes. Capital came from two sources. Backers provided first-loss capital where they absorbed losses first in the event of default, which theoretically aligned their incentives to underwrite carefully. Liquidity providers supplied senior capital into a shared Senior Pool, which sat behind the backers and was only exposed to loss after backer capital was exhausted. The Senior Pool was passive and relied on backers to do the credit work.

The protocol collapsed the incentive structure in a way that backers were compensated primarily in GFI token yield, not in a return that was directly tied to the repayment performance of the pools they approved. The token yield accrued regardless of whether the underlying borrower repaid. This created pressure to approve deals to generate activity and earn yield, not to approve deals because the credit quality justified it. The underwriting function, which is the most critical function in any credit system, was effectively decoupled from the economic consequences of bad underwriting.

When defaults arrived, including Tugende, a motorcycle taxi financing business in Uganda, the protocol had no practical mechanism to recover capital. Tugende operated under Ugandan law. Goldfinch operated as a smart contract on Ethereum. The gap between those two legal realities had no bridge. A token holder in Berlin had no enforceable claim against a defaulted borrower in Kampala. The protocol absorbed the loss, and the design flaw became visible.

Now, the Goldfinch failure is not a failure of the idea, but a failure of incentive architecture and legal infrastructure. Both are solvable. The only issue here was that neither was solved before capital was deployed at scale.

Credix: Credix took the approach of anchoring credit to specific trade receivables. A receivable is a documented claim: a business is owed money by a known counterparty on a known date for a known amount. The risk of a receivable is more bounded than the risk of a general business loan because the repayment source is specific and traceable. If the underlying trade transaction completes, the receivable pays. Thus, the credit analysis is simpler because the collateral is self-liquidating.

Credix built this model primarily in Brazil, where formal invoice documentation is legally mandated and digitised through the Nota Fiscal system. Brazilian businesses generate structured, machine-readable invoices for every commercial transaction above a threshold. That data infrastructure made receivables financing tractable because the receivables were verifiable.

The African problem is that this infrastructure does not exist here at scale. Most Nigerian SMEs do not issue formal invoices. Trade between a wholesaler in Kano and a retailer in Kaduna is documented, if at all, by a handwritten receipt or a WhatsApp message. There is no Nota Fiscal equivalent. A receivables financing model that presupposes formal invoice documentation cannot be imported into a market where that documentation is absent. The model is right, but the data environment is wrong.

Huma Finance: Huma Finance is building in a direction that is architecturally more relevant to Africa than either Goldfinch or Credix. Its premise is that payment history is a credit signal. A business that processes consistent, high-volume payments through a payment rail has demonstrated financial activity that can be used to underwrite a short-term credit facility. The loan is repaid through future payment flows, not through a separate repayment mechanism.

This is the right framework for markets where formal financial records are absent, but transaction activity is high. It mirrors, in structure, what M-Shwari did in Kenya: use mobile money transaction history as a proxy for creditworthiness and extend small credit facilities against it. The difference is that Huma is building on crypto payment rails rather than mobile money rails.

The limitation for Africa is that the payment history Huma currently uses comes predominantly from formalised payment platforms such as crypto payroll processors, stablecoin payment networks, and similar structured environments. The Nigerian SME whose transaction activity is split between cash, mobile money, P2P crypto, and informal trade credit does not have a unified payment rail record that Huma can read. The data is fragmented across systems that do not talk to each other. Until that data aggregation problem is solved, the Huma model works for a narrow slice of the target market.

Building for emerging markets in aggregate is not the same as building for a specific market’s legal system, data environment, and borrower profile. Every protocol I used as an example generalised, but an Africa-specific stack cannot afford to.

The Informal Credit System the Stack Must Reckon With

The blockchain credit stack is not entering a vacuum. African SMEs already have credit infrastructure. It is informal, expensive, and limited in scale, but it functions, and understanding it is a prerequisite for designing a replacement or complement.

The most widespread informal credit mechanism is the rotating savings and credit association, known as esusu or ajo in Yoruba, adashe in Hausa, and isusu in Igbo. A group of known individuals each contributes a fixed amount periodically. The pool rotates to each member in turn. This is a trust-based lending mechanism that operates without a credit bureau because the social penalty for default is immediate and severe. It works because the group size is small enough that every member knows every other member’s reputation.

The second mechanism is trade credit. A supplier who knows a buyer’s reputation will extend goods on credit, to be settled on delivery or within a short cycle. This is the dominant working capital mechanism for Nigerian SMEs, and it operates entirely outside formal financial records. The “credit score” embedded in this system is the trader’s reputation in her network.

The third mechanism is the informal moneylender. Interest rates range from 10% to 30% per month. These rates are not exploitative in the abstract. They reflect the actual cost of unsecured lending without recourse, including the lender’s time, social capital, and the risk of non-repayment. A borrower paying 20% monthly is paying for the absence of the infrastructure that would allow the lender to price risk accurately.

An onchain credit stack that ignores these mechanisms will fail to achieve adoption. The stack must either integrate with them, for instance by tokenising esusu contribution records as a credit signal, or it must offer terms compelling enough to displace them. At 20% per month, that bar is achievable. But it requires acknowledging that the informal system exists and is the primary reference point for the target borrower.

The Credit Stack

The optimal architecture of an onchain credit system for Africa requires four layers:

Layer 0: The Identity Bridge

Onchain transaction history is pseudonymous by default. A wallet address records every transaction it has ever made, but nothing ties that address to a human being in a way that a regulated lender can accept. For an onchain credit score to be portable and lender-acceptable, the wallet must be bound to a verified real-world identity.

In Nigeria, the Bank Verification Number (BVN) and the National Identity Number (NIN) are the two existing biometric identity anchors. Any identity layer for onchain credit in Nigeria must integrate with at least one of them in such a way that there is a cryptographic attestation issued by a trusted identity provider that links a wallet address to a verified identity without exposing the underlying personal data onchain.

Without it, the credit score is unattributable, the collateral is untethered to a legal person, and the loan has no enforceable borrower.

Layer 1: Onchain Credit History as a Score

A trader who has settled hundreds of USDT transactions reliably, on time, across borders, has demonstrated creditworthiness. That history exists onchain. It is tamper-proof, auditable, and portable. The problem is that no one is systematically aggregating and translating that history into a score that a regulated lender will accept.

The inputs to an onchain credit score include: transaction frequency and volume, counterparty diversity, settlement latency relative to agreed terms, repayment history on any prior onchain credit products, and wallet age. These variables are directly analogous to the inputs used by traditional credit bureaus. The difference is that the data is already recorded, permissionlessly, without the borrower needing to have engaged with any formal financial institution.

The bootstrapping problem here would be that a borrower who has not been conducting significant onchain activity has a thin file. The transition period requires a scoring model that can incorporate offline signals: esusu contribution records, trade credit history attested by counterparties, and mobile money transaction data. The score must be calibrated to the African market specifically, not imported from a model trained on US or European borrower data.

Layer 2: Tokenised Real-World Assets

A significant portion of African wealth is locked in assets that formal lenders refuse to recognise: land with customary title, inventory in transit, and agricultural output pre-harvest. Tokenisation does not create value where none exists. It creates a legible, transferable, onchain representation of value that already exists, and it makes that value usable as collateral in a lending transaction.

Land registry tokenisation pilots are running in Ghana and Rwanda. They are moving slowly, partly because the legal question of what a token representing land rights actually confers is unresolved. Let’s not even talk about Nigeria’s Land Use Act and the customary tenure system that presents a harder problem.

What if we look towards Inventory and receivables tokenisation, which is more immediately tractable? A warehouse receipt, a purchase order from a verified buyer, or a bill of lading can be tokenised and used as collateral without requiring resolution of the land tenure problem. These are the assets most relevant to the SME in Aba or Kano who needs working capital against goods she already holds or has already sold.

But then, we also need to look at the legal enforceability problem that applies here. A tokenised asset is only useful as collateral if the lender can actually seize and liquidate it upon default. In Nigeria, this requires either a contractual structure enforceable in court or a smart contract that transfers custody of the asset automatically upon a defined trigger. The second approach is technically cleaner but requires the underlying asset to be in a form that permits automated transfer of custody.

Layer 3: Onchain Lending Without a Branch Manager

Once a borrower has a verified identity, a credit score derived from onchain and attested offline history, and collateral that is tokenised and legible, the lending mechanism itself is the most technically solved part of the stack. Onchain lending protocols can automate underwriting against verified collateral and behavioural history. That way, the cost of origination drops, and the geographic constraint disappears.

But then, what about the capital source question? Who funds the lending side of these protocols for African SME borrowers? The Nigerian diaspora remits approximately $20 billion per year. A portion of that capital, currently sitting in savings accounts in London, Houston, or Toronto, earning near-zero real yield, could earn 15 to 20% annually by funding credit to verified Nigerian SME borrowers, at rates still meaningfully below the 20 to 30% per month that informal lenders charge.

The interest rate arithmetic works, but the trust infrastructure that allows a diaspora lender in London to be confident that the credit score is real, the collateral is legally valid, and the default recovery process has teeth is not.

HARD LEGAL PROBLEMS

The technical architecture described above is buildable, but the hard problems are the legal and regulatory ones.

Enforceability: A credit event has three moments: origination, servicing, and default resolution. The first two can be automated onchain. The third cannot, at present, because it requires a legal system to enforce a claim against a borrower who has not performed. In Nigeria, commercial dispute resolution through the courts is slow. A secured creditor seeking to enforce a charge over collateral can expect years of litigation, not months.

Two approaches exist. The first is contractual design: structure the lending transaction so that the borrower’s obligations are governed by a jurisdiction with faster and more reliable commercial courts, even if the borrower is Nigerian. This is how Eurobond issuers have historically managed Nigerian legal risk. The second is smart contract design: build the collateral custody mechanism so that default triggers an automatic transfer of control without requiring judicial enforcement. This works for digital or tokenised collateral. It does not yet work for physical assets.

The CBN’s Stance: Nigeria’s Central Bank has had a volatile relationship with crypto assets. The 2021 circular prohibited banks from servicing crypto exchanges. The 2023 reversal introduced a licensing framework for Virtual Asset Service Providers (VASPs), but that framework is still evolving. Any onchain credit infrastructure that interacts with Nigerian naira, Nigerian bank accounts, or Nigerian borrowers must sit within this regulatory perimeter or operate in a way that does not trigger it.

Thus, the risk is not that regulators will be hostile indefinitely, but that regulatory uncertainty increases the cost of building, delays institutional participation, and creates compliance overhead that makes the unit economics of small loans harder to justify. The stack must be designed to accommodate regulatory evolution, not to bet on a specific regulatory outcome.

Roadmap of what must be built first

First: identity infrastructure. Nothing else in the stack functions without a reliable, regulatory-compliant mechanism for binding onchain activity to verified real-world identities. BVN or NIN integration with a verifiable credential layer is the unglamorous prerequisite. It is also the one that requires the most regulatory coordination and will therefore take the longest to fully resolve.

Second: credit scoring models calibrated to African transaction data. This requires partnerships with mobile money operators, P2P platforms, and informal group lenders to aggregate transaction history. The models must be trained on African default and repayment data, not transplanted from markets with different borrower profiles.

Third: receivables and inventory tokenisation. Starting with physical RWAs like land is strategically wrong, given Nigeria’s land tenure complexity. Starting with financial claims, invoices, purchase orders, warehouse receipts, is more tractable. The legal framework for the assignment of financial claims is more developed than for land transfer.

Fourth: a pilot lending facility with diaspora capital. A single documented lending cycle demonstrating end-to-end function: identity verified, score computed, collateral locked, loan disbursed, repaid, and collateral released. The pilot does not need to be large. It needs to be rigorous enough to prove that each layer of the stack functions and that the default recovery mechanism has legal teeth.

Fifth: regulatory engagement and licensing. The optimal moment to engage the CBN is after a working pilot, with documented outcomes that can be presented as evidence of controlled operation rather than a theoretical proposal.

CONCLUSION:

To me, Nigeria is the obvious beachhead for this piece because I am a Nigerian, and the stats support it. The SME sector employs 84% of the labour force and contributes nearly 48% of GDP. If onchain credit infrastructure closes even 10% of the $400 billion gap, that is $40 billion in new credit deployed to SMEs that currently have no access to formal capital. At average loan sizes of $10,000 to $50,000, that funds between 800,000 and 4 million credit events. Each credit event generates margin, employment, and tax revenue. The compounding effect over five to ten years would be enormous.

The downstream consequences extend beyond economic output. Formalisation of the informal economy follows credit access. A borrower who has established an onchain credit identity, completed a loan cycle, and built a repayment record has an economic incentive to maintain and improve that record. He/She formalises because formalisation now pays. The credit system becomes the mechanism of economic inclusion, not the certificate of formal participation.

What does not exist yet is the integration: a stack that pulls onchain transaction history, maps it to a score against a verified identity, accepts tokenised real-world assets as collateral, routes the loan through a protocol that settles without a correspondent bank, and enforces default recovery within a legally functional framework. That full stack, built for the African market specifically, by people who understand what it costs to run a business here without a bank that will back you, is the most important thing this industry could build on this continent.

Technova reminded me that the people asking the right questions are already here. The builders need to catch up.

Want to read more?

https://www.pwc.com/ng/en/assets/pdf/pwc-msme-survey-report-2024.pdf

https://www.smefinanceforum.org/sites/default/files/Data%20Sites%20downloads/IFC%20Report_MAIN%20Final%203%2025.pdf

https://research.contrary.com/company/goldfinch

https://fatefoundation.org/wp-content/uploads/2024/03/7.-SMEDAN-1.pdf

https://www.cbn.gov.ng/Out/2024/CCD/CBN%20Records%20Highest%20Remittances.pdf

https://upcommons.upc.edu/server/api/core/bitstreams/f895f9c7-46de-428f-a7a7-f82174b733ea/content

https://www.imtfi.uci.edu/files/docs/2015/M-Shwari%20Final%20Report_Final-Feb%2028%202017-CLN.pdf

https://www.afdb.org/fileadmin/uploads/afdb/Documents/Publications/00157616-FR-ERP-41.PDF

My mentor is back on a roll

How about adoption issues for them

On chain credit scoring… how do we verify who is who?

A high volume of transactions could be just a retail p2p trader without any verifiable business that’s worth a bankable score.

Onchain data mainly shows volume not intent.

For banks to verify the source of money to give a person a good credit score using onchain data, there has to be a lot of identity and business verifications, so as to know if for sure they worth the score, and that brings up the issue of privacy for some people.

Infact most people, cause now their money can be fully tracked and taxed.