To what degree is FXS undervalued?

To what degree is FXS undervalued?

A tldr on Ouroboros Capital' Bull Case For Frax Finance

Frax Finance operates on a sophisticated mechanism of collateralized debt positions (CDPs), enabling the maintenance of its peg to the US dollar. The protocol stands out by allowing users to mint FRAX tokens by collateralizing popular stablecoins like USDC or DAI. This inclusive approach broadens access to Frax for individuals who may not possess other stablecoin options, such as USDT.

While Frax Finance has received accolades for its groundbreaking stablecoin issuance model, it has also encountered criticism due to its inherent complexity and the associated risk of instability. Notably, in March 2022, the protocol experienced a depeg event when the FRAX price dipped below $0.90. The occurrence resulted from a combination of factors, including a substantial sell-off of FRAX tokens and a shortage of collateral within the CDP system.

Despite the depeg event, Frax Finance has demonstrated remarkable resilience and sustained growth in popularity. As of March 2023, FRAX boasts a market capitalization surpassing $1 billion, solidifying its position as one of the most sought-after decentralized stablecoins globally.

In light of Frax Finance's evolving trajectory, Ouroboros Capital meticulously presents an investment thesis focused on FXS, the protocol's native token.

In today’s article, i’ll try to provide a concise overview of the report, delving into key aspects such as the investment thesis itself, and offering key insights into the investment potential of FXS within the rapidly evolving crypto/defi space.

Ouroboros Capital's Investment Thesis

Ouroboros Capital’ investment thesis for FXS is based on its valuation support and the anticipated significant incremental value the market is likely to attribute to the token in the near future.

Ouroboros Capital is bullish on FXS for a number of reasons…

First, they believe that Frax Finance is a well-designed protocol with a strong team. The protocol has been audited by several reputable firms, and the team has a proven track record of success in the DeFi space.

Second, Ouroboros Capital believes that FXS is undervalued. The token is currently trading at a significant discount to its intrinsic value, which is based on the protocol's seigniorage revenue.

Third, Ouroboros Capital believes that FXS has a large addressable market. Frax Finance is one of the leading decentralized stablecoin protocols, and the market for stablecoins is growing rapidly.

Value Accruals:

Frax generates approximately $20 million in annualized revenue, indicating its strong revenue-generating capability.

The protocol fee structure of Frax allocates 90% of staking yield to sfrxETH stakers, with the remaining 10% divided between the protocol treasury and a slashing insurance fund.

The revenue generated from frxETH, once it catches up to rETH TVL, is expected to be around $8 million per year.

The Automatic Market Operations (AMOs) within Frax play a crucial role in maintaining peg stability and generating revenue by utilizing protocol-owned liquidity.

The major AMOs, including Curve/Convex AMO, frxETH AMO, and FraxLend, are estimated to generate approximately $14 million in revenue, primarily in the form of $CRV and $CVX tokens. The combined revenue from all AMOs is expected to be closer to $16 million.

The future value accrual driver, Fraxchain, is anticipated to launch before 2024 and will allow native Frax assets to be used as gas. This is expected to contribute indirectly to the value accrual through frxETH and the Frax stablecoin.

Fraxchain's gas fees are estimated to be approximately $5,000 per day ($1.8 million per year), which would account for around 10% of the current protocol fees. Additionally, the market is likely to assign significant incremental market cap to FXS due to Fraxchain's introduction.

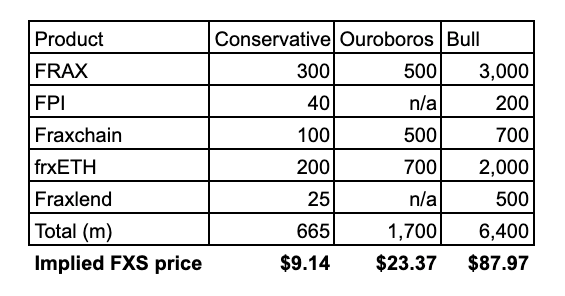

Valuation:

While traditional valuation models may not be suitable for crypto assets, the report provides a valuation exercise that estimates the market cap of FXS.

The valuation is divided into three parts:

Frax the Stablecoin

frxETH, and

FraxChain

The conservative valuation suggests a market cap range of $600 million to $1.7 billion, while the more bullish scenario predicts a range of $1.5 billion to $2.2 billion.

These estimates highlight the potential for significant value appreciation.

Key narratives about FXS:

The growth of the decentralized stablecoin market: The decentralized stablecoin market is growing rapidly, as more and more users look for alternatives to centralized stablecoins like Tether (USDT) and USD Coin (USDC). Frax Finance is one of the leading decentralized stablecoin protocols, and it is well-positioned to capture a significant share of this growing market.

The importance of seigniorage revenue: Seigniorage profits on Frax Finance are generated when the protocol mints new FRAX stablecoins. For each FRAX minted, the protocol burns a corresponding amount of FXS tokens. The amount of FXS burned is equal to the seigniorage profit. For example, if the protocol mints 100 FRAX, it will burn 100 FXS tokens. The seigniorage profit is therefore 100 FXS tokens. The seigniorage profit is then distributed to FXS holders in proportion to their FXS holdings. This means that FXS holders are rewarded for holding the token, even if the price of FRAX remains stable. Ouroboros Capital believes that seigniorage revenue is a key driver of FXS's value, and they expect this revenue to grow in the future as the protocol's user base expands.

The governance token: FXS is a governance token that gives holders the right to vote on protocol decisions and receive a portion of the protocol's seigniorage revenue. Ouroboros Capital believes that this gives FXS holders a strong incentive to support the protocol and its growth.

FXS is a scarce asset with a growing demand. The total supply of FXS is capped at 100 million tokens, and it is burned whenever new FRAX is minted. This means that the supply of FXS is becoming increasingly scarce over time. In addition, the demand for FXS is growing as more users adopt Frax Finance.

FXS is a yield-generating asset. FXS holders can earn yield by staking their tokens in the Frax Finance protocol. The current yield on FXS is around 30% APR, and it is expected to continue to grow as the protocol matures.

FXS is a governance token with the potential to appreciate in value. FXS holders have the right to vote on protocol changes, and they can also propose new changes. This gives FXS holders a lot of control over the future of Frax Finance.

MythBusters:

Myth 1: FRAX is at risk of a death spiral.

Buster: This is false. The protocol has significant collateral, with $237mn in stablecoin equivalent assets and $37mn in volatile assets, backing $300mn of non-POL FRAX in circulation. There is no risk of a death spiral.

Myth 2: The US-based team exposes Frax to regulatory risks.

Buster: This is false. The deployment of FrxGov will transfer control of the protocol to veFXS holders, eliminating centralized operational elements and mitigating regulatory threats.

Myth 3: Frax lacks innovation and is a combination of existing forks.

Buster: This is false. Frax incorporates unique innovative features. If it lacked innovation, it on’t have had the ability to enhance and expand upon its existing Frax product.

Conclusion:

The report asserts that FXS presents an asymmetric risk:reward opportunity for investors. The anticipated catalysts, including frxETH adoption, FraxChain launch, Frax v3, and frxGov implementation, provide a positive outlook for value accrual and potential market cap appreciation.

From my end, i’d say that the team's track record and commitment to development further strengthen the investment thesis. FXS has significant growth potential and should definitely be considered as one of the highest conviction ideas within the crypto space.