Frax v3 Vs MakerDao's DSR

Frax v3 Vs MakerDao's DSR

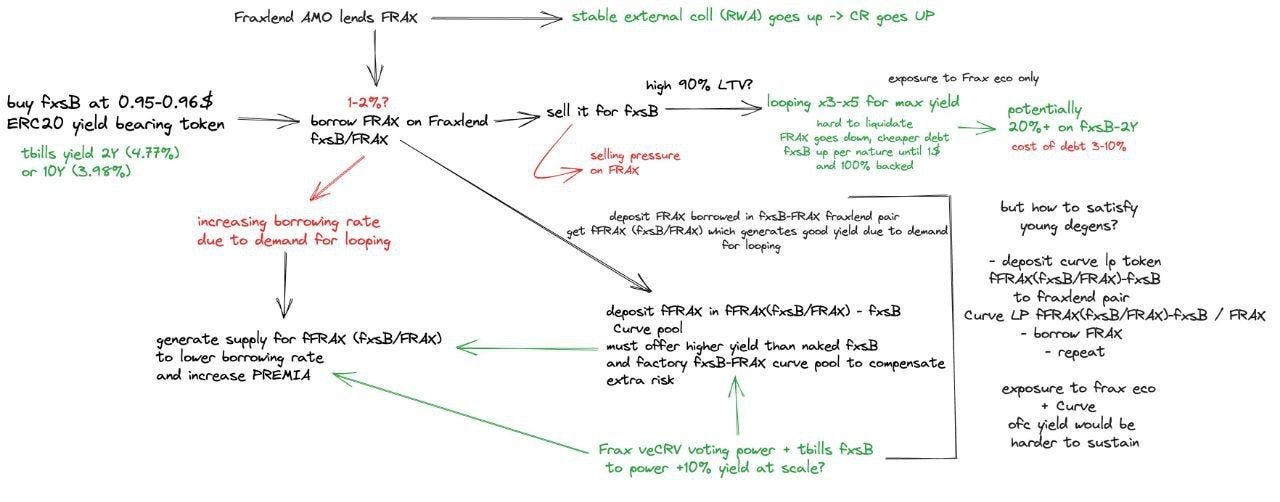

FXBs as a game-changing yield opportunity

On the Frax Finance Telegram GC, the chatter is about the possibility of staking Frax to earn impressive yields. But what's the scoop on this exciting development?

The answer lies in the remarkable versatility of FXB tokens, which hints at the potential for some serious yield generation. In fact, it's poised to give MakerDAO's DSR (Dai Savings Rate) a run for its money.

To really understand all these, we first have to understand Maker DSR…

The Maker Dai Savings Rate (DSR) is a critical component of the MakerDAO ecosystem, designed to provide users with the opportunity to earn interest on their Dai holdings while contributing to the stability of the Dai stablecoin.

The Maker DSR allows individuals who hold Dai to lock their Dai tokens into a DSR contract, effectively "staking" their Dai. When Dai is locked into the DSR, it continuously accrues interest based on a global system variable known as the DSR. This interest is earned passively, and there are no specific restrictions or fees for using the DSR beyond the gas fees incurred when locking and unlocking Dai.

The interest rate earned through the DSR is determined by the DSR rate. For instance, if the DSR rate is set at 2%, a user who locks 100 Dai into DSR mode and keeps it locked for a full year would earn two additional Dai. These earnings are automatically added to the user's wallet when they unlock their Dai.

The DSR serves a crucial role in the MakerDAO ecosystem by creating incentives for individuals to either lock or unlock their Dai holdings based on market conditions. This mechanism helps balance the supply and demand for Dai in the ecosystem, ensuring its stability.

The DSR is funded through the Stability Fees collected from Collateralized Debt Positions (CDPs) within the MakerDAO system. For instance, if the average Stability Fees collected on CDPs is 3%, a portion of these fees could be allocated to fund the DSR, even if the DSR rate is set at a lower percentage, such as 2%.

MakerDAO's DSR has been a popular choice for those looking to earn a yield in the DeFi space, offering returns in the range of 3% to 5%. However, Frax is quietly building a robust contender, and it's about to make some noise.

Let's dive into the specifics of FXB yields.

Intended Mechanics of FXB

FraxBonds are decentralized utility tokens that represent debt in FRAX stablecoins at a specific timestamp. This means FRAX holders can reserve discounted future access to FRAX.

The technique is straightforward yet effective: consumers can subsequently buy $1 worth of FRAX for a price less than its face value. This means users have a rare chance to protect themselves against prospective price changes and ensure future worth with this strategy.

The protocol assumes ownership of the collateral upon purchase of FraxBonds, ensuring that the funds are available to pay off the loan within the allotted time frame. These bonds aren't merely a static investment because, at the specified maturity dates, they transform into FRAX automatically, giving users a seamless experience.

FraxBonds come in a variety of terms, including 1, 2, 3, or 4 years. According to the idea of traditional bond maturity, the annual conversion takes place on January 1st of every year.

By introducing these bonds, Frax is able to bring the yield curve onto the blockchain, giving customers a broad selection of investment alternatives spanning several years.

Yield time?

Frax has strategically leveraged the Curve flywheel, positioning FXB tokens to potentially generate an impressive Annual Percentage Yield (APY) ranging from 6% to 8%.

To put this into perspective, U.S. treasuries currently yield around 5.25%, and when you factor in CRV, CVX, and FXS emissions, the potential returns become even more appealing.

But here's where things get truly interesting. What if I told you that Frax holders might have the opportunity to leverage their yields to a significant extent?

While this may sound like a bold move, it could be a game-changer.

Imagine capitalizing on that robust 8% yield by amplifying it up to 9x through platforms like Fraxlend, BAMM, or Curve's LLAMA Lending market, all while incorporating soft liquidations for added safety.

This opens the door to what some are calling "conservative degeneracy."

Conservative degeneracy is often used to describe a relatively cautious approach to speculative or high-risk investments. It may seem contradictory because "conservative" typically implies a low-risk approach, while "degeneracy" is associated with high-risk behaviour. But why won’t we call this conservative degeneracy when initial estimates even suggest that potential APYs could skyrocket, ranging from a staggering 15% to as high as 25% when FXBs are utilized in this fashion?

While it may have been a relatively slow week for Frax news, the pieces of information that have surfaced are undeniably game-changing. It's clear that they have the potential to redefine how we think about yield generation in the crypto space.